Update your subscriptions for Grant Thornton publications and events.

European regulatory authorities have introduced new legislation, referred to as the Investment Firms Regulation EU 2019/2033 (‘IFR’) and Investment Firms Directive EU 2019/2034 (‘IFD’), which aims to establish a tailored prudential framework for investment firms.

Contents

Subscribe to our mailing list

This is the fifth publication in a series of articles by Grant Thornton and focusses on the impact of the prudential consolidation for investment firms.

The new prudential regime makes changes to the prudential consolidation for investment Firm Groups. The purpose of these new requirements is to ensure that investment firms are consolidated in an appropriate way to ensure that there is consistency across the European Union. Prudential Consolidation under the new regime should only be considered under the IFR when the Investment Firm group contains multiple regulated entities within the European Union.

Investment Firm groups are made up of a consolidating entity or a “Union Parent” and appropriate regulated consolidated entities. It is important to note that the new prudential regime includes entities outside the EU within the investment firm group with regard to consolidated capital and liquidity requirements and reporting.

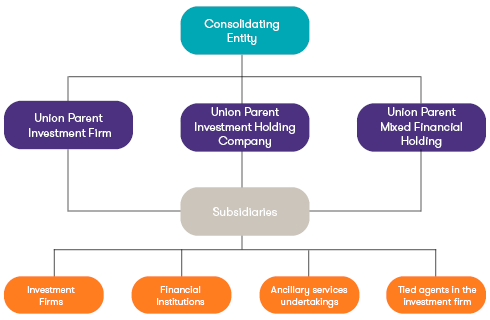

Consolidating Entity

According to recital 1 of the Draft RTS (EBA/CP/2020/06) on prudential consolidation of investment firm groups (‘Draft RTS’), consolidation is to be carried out at the highest level of the group within the European Union. This draft guidance is pending the final RTS on prudential consolidation of Investment Firms Groups.

Under the prudential consolidation in the new prudential regime there are three types of entities that can be considered the consolidating or Union parent undertaking:

- Union Parent Investment Firm;

- Union Parent Investment Holding Company; and,

- Union Parent Mixed Financial Holding Company.

Figure 1. Types of parent and consolidated entities as per Section 3.11 of the Draft RTS on the methods of prudential consolidation of investment firms

As per Recital 5 and Article 2.1 of the Draft RTS, all regulated entities included within the consolidated financial statements are to be included within the consolidation perimeter. The entities can only be one of the four following regulated entities as specified in figure 2 above:

- Investment Firms;

- Financial institutions;

- Ancillary services undertakings; and,

- Tied agents in the investment firm.

It is noted that the above list can contain entities outside the EU. Those entities would not be subject to the IFR and IFD on an individual basis, however they must be considered within the groups consolidated capital requirements as outlined below. The investment firm regime is not applicable to unregulated entities or an entity not classified as one of the above four entity types.

For Investment Firm groups wherein the parent entity is situated in the United Kingdom, the group may be subject to prudential consolidation under the Financial Conduct Authority’s (‘FCA’) Investment Firms Prudential Regime. The FCA’s regime is similar in nature to the European regime, however, the investment Firm group should ensure appropriate analysis of the FCA regulatory text is undertaken.

Own Funds calculation methodology

The largest impact that prudential consolidation will have for many firms will be the capital requirement implications. As such the own funds requirements for Investment Firm groups are outlined below. Please see our earlier publication on Capital Requirements K-Factors for further information on own funds requirements under the IFR.

The group’s own funds requirements amounts to the highest of the following three requirements

The fixed overheads requirement

As per article 9 (1) of the Draft RTS, the consolidated fixed overheads requirement shall amount to at least one quarter of the consolidated fixed overheads of the Union parent undertaking of the preceding year on a consolidated basis.

The permanent minimum capital requirement

As per article 10 (1) of the Draft RTS the permanent minimum capital requirement at the individual level of all group undertakings that are fully consolidated.

The K Factor requirement

In line with Article 11 of the Draft RTS, the group consolidated K-factor requirement shall be calculated by adding together all different K-factors requirements calculated on a consolidated basis. This aggregation is subject to certain intragroup implications as outlined in the draft RTS.

Derogation opportunities

An Investment firm group may avail of the group capital test as specified in article 8 of the IFR. The group capital test can serve as a derogation from the requirement for an investment firm group to have to comply with all the obligations of prudential consolidation. If the group passes the group capital test a competent authority may allow derogations with regard to consolidated capital and liquidity requirements.

Under the Group capital test, the Union parent investment firms, Union parent investment holding companies, Union parent mixed financial holding companies and any other parent undertakings that are investment firms, financial institutions, ancillary services undertakings or tied agents in the investment firm group shall hold at least enough own funds instruments to cover the sum of the following:

- the sum of the full book value of all of their holdings, subordinated claims and instruments; and

- the total amount of all of their contingent liabilities in favour of investment firms, financial institutions, ancillary

How Grant Thornton can help

Grant Thornton’s Financial Services Risk, Consulting and Advisory teams currently support a number of investment firms with understanding, preparing for and implementing the new prudential framework in a practical hands-on manner. In particular, our IFR/IFD experts have extensive knowledge of the relevant legislation and guidance and the challenges these pose to your firm. Our experience includes establishing multiple Investment Firm group perimeter’s for European and Cross border groups, in addition to calculating the consolidated capital and liquidity requirements of multiple Investment Firm Groups.

Our IFR/IFD experts can help your firm assess its prudential consolidation status arising from the new regime and advise on methods to ensure full compliance balanced with your business needs and tight implementation timelines.

Authors

-

Dwayne Price

Dwayne joined Grant Thornton in 2016 as partner to head our Regulatory Advisory Services offering. Dwayne leads the firm’s risk and regulatory offering focusing on Quantitative Risk Advisory, Regulatory Risk and Strategy, and Regulatory Support services.View Profile