The UK’s withdrawal from the EU, has not affected the rights of Irish and UK citizens within the Common Travel Area (CTA). They are still able to move freely and reside in either jurisdiction while enjoying associated rights and entitlements such as access to employment, healthcare, education and social benefits. Irish nationals and other EU nationals also maintain their freedom of movement within the remaining EU Member States. This means that Brexit may not have an immediate impact on Irish employers with regards to the movement of certain employees. However, many employers will have to deal with global mobility and immigration concerns due to Brexit.

How can employers mitigate risk?

![How can employers migitate risk.png]()

Social Security

Social Welfare (Convention on Social Security between the Government of Ireland and the Government of the United Kingdom of Great Britain and Northern Ireland) Order 2020 came into effect on 1 January 2021. It ensures that Irish and UK citizens maintain the same social security rights and entitlements under the Common Travel Area arrangements, after the UK left the EU. This convention is similar to the EU social security coordination system, ensuring that employees still only pay social security contributions in one country.

The EU-UK Trade and Cooperation Agreement included a protocol on Social Security Coordination, which ensures that EU and UK citizens moving between member states will only have to pay social security in one country at a time. It includes provisions for ‘Detached Workers’, who can remain in their “home” social security system while temporarily working abroad. In February all EU countries opted in to the ‘Detached Workers’ rules. Separate rules apply to workers between the UK and the EFTA countries; Norway, Iceland, Liechtenstein and Switzerland.

Employers will need to know the citizenship status of their employees, where they carry out work duties and to make applications if necessary, under the revised rules to the relevant social security authority.

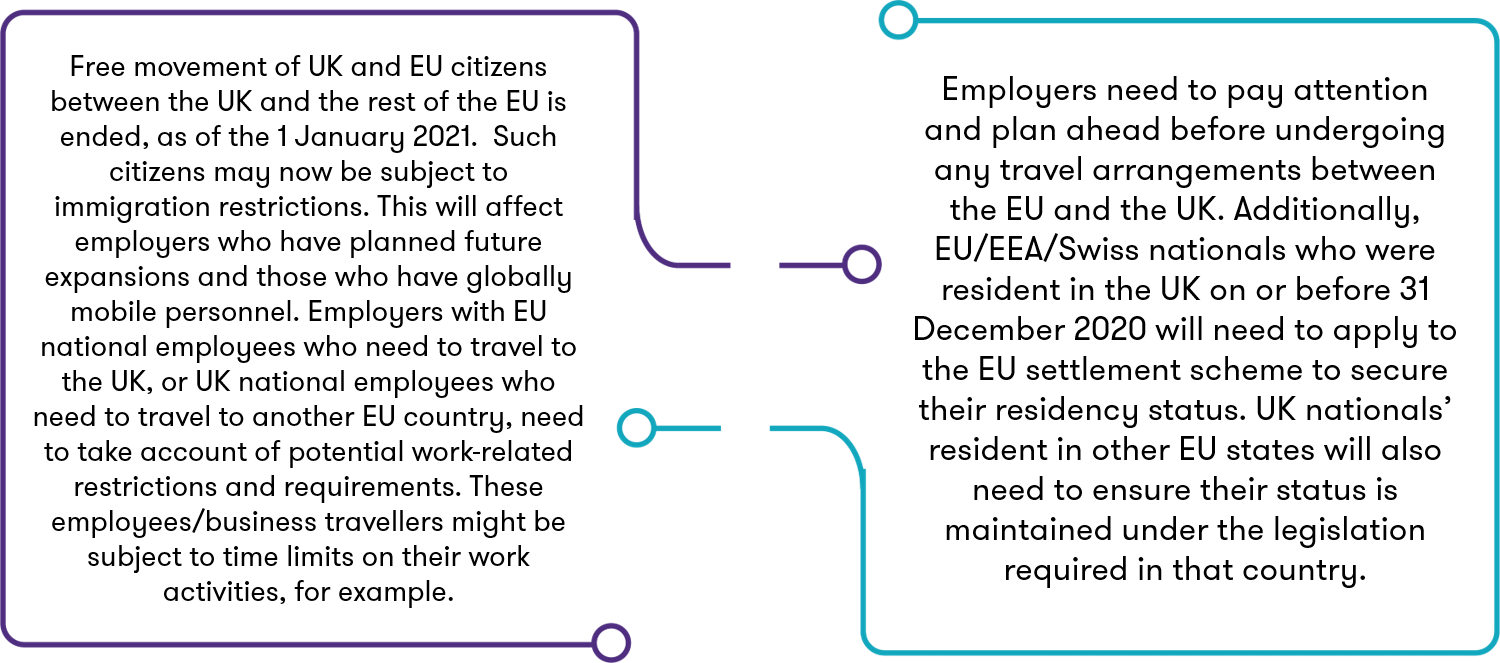

Personnel Mobility Matters

Brexit has not changed the underlying tax rules in Ireland but there could be an increase in short term business visits between Ireland and the UK, due to the close business relations and geographic proximity. This could result in tax implications for many individuals who would be considered as Short Term Business Visitors (STBV’s). They may have Irish PAYE obligations based on their individual Irish workdays. Revenue has provided extensive guidance on STBV matters.

UK employers may be liable for potential Irish PAYE obligations depending on their employees’ travel patterns, duties carried out and duration of those work activities.

Employer advice

We encourage employers to review their workforce to identify any employees who could be affected by immigration restrictions.

You should:

- Assess your global mobility procedures, planning ahead and integrating immigration requirements and pre-travel processes.

- Ensure that your key stakeholders understand the impact the new requirements will have on the business. If required, promote the benefits of upskilling on immigration requirements.

- Communicate with your employees, making them aware of any new pre-travel requirements or steps to secure settlement.

- Analyse the potential cost impact of attaining required immigration authorisation for employees.

How Grant Thornton can help

Our specialist employment tax team can assist you in addressing the challenges imposed by Brexit and mitigate any risks and costs.

See our Global Mobility Services offering See our Employer Solutions offering

![Subscribe button.jpg]()