Sign up for expert insights, industry trends, and key updates—delivered straight to you.

Pre-Legislative Scrutiny of the General Scheme of the Central Bank Individual Accountability Framework Bill – April 2022.

Contents

Stay informed with the latest insights, news & events

Background

The proposed legislation follows on from the reforms proposed in the Central Bank’s report on Behaviour and Culture of the Irish Retail Banks published in 2018, which highlighted the shortcomings in the culture of Irish retail banks. The Central Bank has emphasised that there has been a focus both nationally and internationally since the global financial crisis on “strengthening corporate culture, driving positive behaviour and increasing individual accountability”. In this report, the Central Bank found that in its Tracker Mortgage Examination, there were significant “cultural failings within the banking sector… …in addition to poor systems, weak internal controls and poor governance, caused detrimental and, in some cases, devastating impacts on consumers”.

In response to this report, the Government made a commitment in the 2020 Programme for Government to introduce a Senior Executive Accountability Regime (SEAR) in order to engender the desired positive culture change and heightened accountability in regulated financial service providers (RFSPs) and as such to provide them with the tools on which a positive culture could be built.

The general scheme broadly reflects the proposals as set out in the Behaviour and Culture Report into Irish Retail Banks, while also drawing on the experiences of the implementation of the UK’s senior management regime, which has also been implemented in Australia and Singapore. It was noted that Ireland will be the first country in the EU to introduce such a scheme.

The Committee decided to undertake pre legislative scrutiny of the general scheme by holding meetings on 3rd and 10th November 2021 with the Central Bank and the Minister for Finance. It also sought written submissions from the Banking and Payments Federation of Ireland (BPFI) and the Irish Banking Culture Board (IBCB).

Submissions Received

- Banking and Payments Federation of Ireland Submission: In its submission the BPFI detailed 15 areas where it has requested further clarity and guidance from the Central Bank with regard to the general scheme (see Appendix 1). The most pertinent of these related to clarification around “reasonable steps”, “responsibility maps”, and “conduct standards”. The BPFI welcomed the alignment of senior executive functions (SEFs) to the list of pre-approved controlled functions (PCFs) as prescribed by the Central Bank, but it believes that there needs to be an element of flexibility to allow firms structure their senior management teams in a way that optimises resources and talent. It also emphasised, the dangers which may arise if applying the SEAR to interim role holders, as excessive or disproportionate.

- Irish Banking Culture Board Submission: In its submission the IBCB advocates that its members are in full support of the general scheme as they believe individual accountability is the cornerstone of positive behaviour and culture in the financial services sector. The IBCB commented on four main aspects:

-

- The need for the IAF to be framed as promoting positive behaviour in favour of the focus on the punitive aspects;

- The importance of consultation and engagement between the Central Bank and the regulated financial service providers (RFSPs);

- The opportunity for the IAF to contribute to the restoration of trust in the financial services sector and;

- The need to reflect on the internal controls and corporate governance within firms to incentivise good behaviours. The IBCB recommends that while guidance is required in order for firms to implement the IAF, an element of flexibility is imbued in the process to accommodate individual firm’s governance arrangements. The IBCB makes the point that the IAF in either primary or secondary legislation, must set out the relationship between collective and individual accountability and determine where responsibility lies for the use of artificial intelligence and machine learning, although the latter point is not specifically addressed in the general scheme. The IBCB concludes that the implementation of an Individual Accountability Framework is an opportunity for both the regulator and the regulated in the financial services sector.

Comments and Recommendations

Responsibility Maps

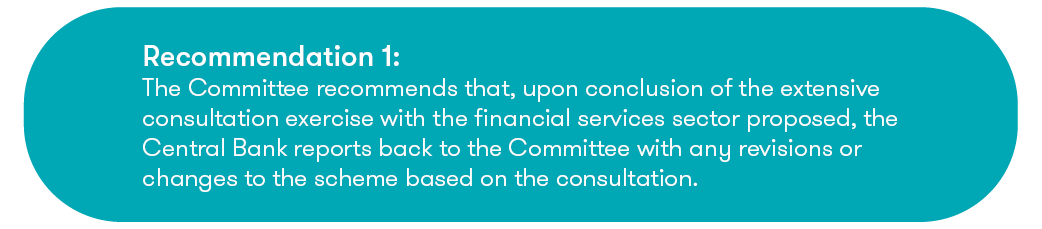

The BPFI’s submission requests further clarification around the statement of responsibilities such as the “key elements of each role and the responsibilities and expectations of the office holder”. While further guidance would be welcome, the Committee accepts that there will be a significant engagement and consultation with stakeholders from the financial services sector following the commencement of the legislation. The Committee, therefore, would be obliged if the Department could furnish the Committee with a report on this consultation following its conclusion. The Committee is in support of the proposed responsibility mapping and is of the opinion that it would have a significant impact on increased individual accountability.

Scope of SEAR

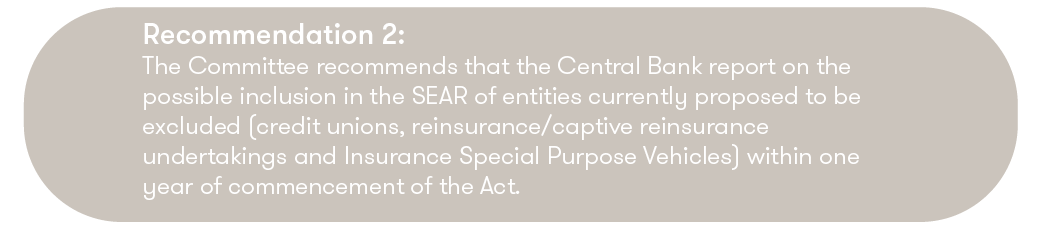

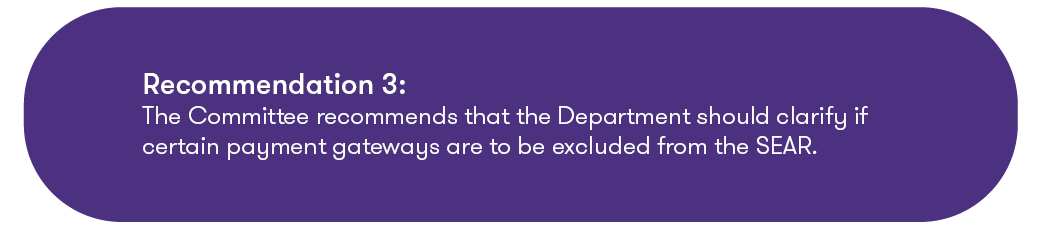

In terms of the scope of firms included in the SEAR, it is envisaged that credit unions, insurance undertakings, investment firms (which underwrite on a firm commitment basis and/or deal on their own account and/or are authorised to hold client monies/assets) and third country branches of same would be excluded. It is clear that this does not encompass all the financial institutions that could potentially be included and that the position may change and evolve over time. As such, the Committee recommends that the Central Bank report within one year of commencement of the legislation on the status of the currently excluded institutions. With regard to third country branches included in the regime, as the BPFI requested, clarification is required on whether the intention is to include Irish firms operating in other jurisdictions or firms from outside of Ireland operating with branches in the country. The third recommendation in this section relates to financial technology firms, specifically payment gateway services and their potential inclusion in the SEAR.

Reasonable Steps

The general scheme proposes to unite the PCF’s with Senior Executive Functions (SEFs) to whom the SEAR is applicable. These SEFs would include board members, executives reporting directly to the board and heads of critical business areas. Senior individuals within the organisation will be required to take “reasonable steps” to avoid their firm contravening legal and regulatory requirements in the business area for which they are responsible. The Central Bank at its appearance before the Committee confirmed that despite an overall desire for clarity with regard to what exactly is meant by “reasonable steps”, and that the regime will be clear and demanding, it is purposefully flexible to allow it to fit the range of the institutions to which it will apply.

Appendix 1 – BPFI Submission

Areas on which individuals, within BPFI member institutions, will need clarity and guidance include:

- The scope of their specific regulatory responsibilities.

- What is a “reasonable step”and what is a complete set of reasonable steps for each SEF and/or prescribed responsibility. How will the Framework/ SEAR apply to RFSPS which are subsidiaries of a parent RFSPS, in particular, in respect of outsourcing arrangements between parent and subsidiary institutions where functions are being performed at group level by the parent institution.

- Will the PCF list be further expanded?

- The extent to which individuals can be held accountable for the actions/ failures of others and how this differs depending on whether the actions/ failures of others are within or without the direct oversight of those individuals.

- How firms can share prescribed responsibilities and the expectation of those that share prescribed responsibilities.

- How the Framework will apply in relation to PCF to PCF reporting (i.e., where a PCF reports to another PCF and, therefore, the more senior PCF has oversight).

- The expectations of firms when developing their management responsibility maps with respect to content, sections, length – to ensure that there is consistency across firms and that the requirements of the CBI are satisfied and that the documents are useful for firms’ management and compliance.

- How will the CBI ensure that there is a common approach within financial institutions to SEAR whilst acknowledging that the structure and content of responsibility maps will be adopted by individual institutions.

- What constitutes a conduct standard breach to ensure that there is consistency of application of treatment and disciplinary action taken across firms such that employees are not disadvantaged due to a lack of consistency in approaches across industry.

- The intended approach for the reporting of breaches of Conduct Standards to the CBI; the threshold for breaches of conduct rules and the level of materiality.

- The fact that the Framework must be clear that a statement of responsibility is specific to the individual role holder rather than to the PCF/ SEF role as a function, as each individual is likely to bring different responsibilities, above the prescribed responsibilities, to their roles.

- What will be the impact of the Framework on BPFI members’ outsourced service providers and how will such arrangements be reflected in “reasonable steps”?

- How will the Framework apply to external foreign branches of Irish RFSPs, non- RFSPs, subsidiaries and third country branches operating in Ireland?

- Timeframe for training and implementation - will there be phased implementation of the various elements of the Framework?

- The intended approach to retrospectivity and how the enforcement powers will apply in relation to issues which are historic, but continuing, when the new Framework becomes effective.

Authors

-

Amanda Ward

Amanda joined Grant Thornton in August 2020 as a Partner in our Consulting team. Prior to joining Grant Thornton Amanda spent 8 years with the Irish branch of an International Nordic Bank finishing in the role of Chief Operating Officer. Prior to this she spent 8 years with a Big Four firm where she worked with the Financial Effectiveness Consulting and Audit divisions.View Profile -

Kevin Coleman

Kevin is an established regulatory and risk leader with over 21 years’ financial services regulation and risk experience. Kevin leads our financial services consulting offering in conduct and prudential risk and has worked on all sides of the table as a former banker, leading advisor and as a former senior regulator.View Profile