Sign up for expert insights, industry trends, and key updates—delivered straight to you.

Contents

Stay informed with the latest insights, news & events

Introduction

The European Insurance and Occupational Pensions Authority (“EIOPA”) recently issued an opinion on the supervision of captive (re)insurance undertakings (“captives”) to guide National Competent Authorities (“NCAs”) with the supervision of these undertakings. The guidance specifically relates to intra-group transactions and governance arrangements.

Whilst EIOPA acknowledges that Solvency II makes note of the unique nature of captives they also stress a need for a balanced approach concerning managing cash pooling arrangements captives participate in, alongside maintaining a robust governance policy through adequate outsourcing of key functions whilst adhering to Solvency II requirements.

Cash pooling arrangements

Cash pooling refers to intra-group arrangements for sharing liquidity among entities to manage cash within the group effectively. Under these agreements, entities with surplus liquidity would typically receive interest from those with negative balances. These agreements are attractive, since the net interest received by the group on the net cash balance could be greater than what would be received if the cash was held by each individual entity on a segregated basis.

Risk management considerations

EIOPA has identified a number of risks with these arrangements including that the interest rates are not at arm’s length, concentration risk, default risk, and liquidity risk in the event of the insolvency of the parent company or other pool participants.

The level of risk a captive is exposed to will depend on the structure of the cash pooling arrangement:

- Physical cash pooling: Surplus liquidity is transferred to a master account, creating an inter-company transaction.

- Notional cash pooling: Positions are virtually consolidated without real liquidity transfer.

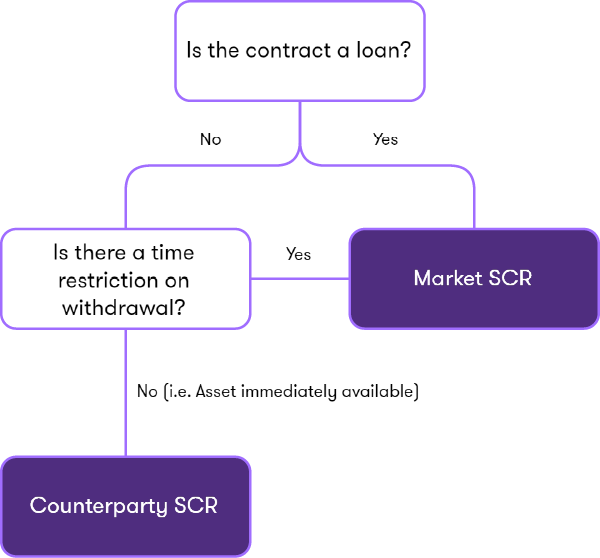

Captives should take care to classify assets and liabilities according to the economic substance of the cash pooling arrangement and to determine whether assets should be treated as loans or cash at bank. This determination will influence the treatment of the asset when the captive is calculating their Solvency Capital Requirement (“SCR”) as demonstrated in the figure below:

Captives should also ensure that they are applying the correct credit rating of counterparties involved in the cash pooling arrangements. If a counterparty is unrated, the probability of default should be based on "unrated" credit exposure. However, the rating of the parent company can only be used with a letter of credit, guarantee, or equivalent arrangement has been provided.

It’s important for captives to assess all risks and benefits of these arrangements, including the impact on liquidity and concentration risks. They should also appropriately reflect material reliance on these transactions in the Own Risk and Solvency Assessment and evaluate risk exposures based on stress scenarios.

Application of the prudent person principle

Insurance and reinsurance undertakings invest all their assets in accordance with the prudent person principle, which generally requires them to only invest in assets and instruments whose risks they can properly identify, measure, monitor, manage, control and report. They should also appropriately consider the impact of the investments on the captive’s overall solvency needs.

Captives should still adhere to the prudent person principle when entering into cash pooling arrangements, specifically considering the following:

- Security and Quality: unrated assets should reflect the lack of information on credit quality and the creditworthiness and number of different counterparties should be considered.

- Liquidity and Availability: the duration and conditions on withdrawal of the cash pooling arrangements and potential guarantees by the cash pool leader should be assessed.

- Profitability: the profitability of cash pooling arrangements in the context of the macroeconomic situation should be evaluated.

- Asset-Liability Management: the duration (mis)matching and cash-flow matching rules in cash pooling arrangements should be considered.

- Conflict of Interest: transactions should reflect the best interests of policyholders, and arm’s length pricing should be considered if necessary.

- Diversification: adequate portfolio diversification should be demonstrated considering the risk profile of the undertaking.

These principles are consistent with the Central Bank of Ireland’s expectations outlined in CP150 relating to intra-group transactions that require groups to ensure that the review and monitoring of intra-group transactions is adequately applied at (re)insurer level and that there is no undue influence or control from the group or overreliance on group practices, policies and procedures.

Governance arrangements

EIOPA have recognised that there are peculiar aspects related to the business model of captives which could lead to regulation being applied proportionally. However, they have stated at the Administrative, Management, or Supervisory Body (“AMSB”) of the captive as a whole should possess the necessary seniority, qualifications, competency, skills and professional experience. EIOPA have noted that there should be no exception from this requirement for captives.

Captives are allowed to outsource key functions. The captive must designate a person with the overall responsibility for the outsourced key function who is fit and proper and has sufficient knowledge and experience regarding the outsourced key function to be able to challenge the performance and results of the service provider. This person can be:

- An employee of the captive (re)insurance undertaking.

- A person under NCA supervision with a link to the undertaking via a dedicated committee.

- An employee of a company within the same group, properly documented in outsourcing arrangements.

Captives should ensure that there are safeguards in place to mitigate conflicts of interest and operational risks associate with outsourcing. They should also ensure that there is clear documentation of the segregation of duties where multiple services are provided by the same service provider and conduct. Finally captives should ensure that they perform and document initial and ongoing due diligence on outsourced service providers.

How we can help you

We boast both an Actuarial and an Insurance team that has significant industry and regulatory experience regarding the items mentioned in the above article, making us well-placed to understand the regulatory requirements and the implications of these on captives and NCAs.

We can provide tailored expertise that spans the full range of various insurance sectors, and our global reach allows us to bring an array of international experience on behalf of our Irish-based clients to help you with practical solutions for your needs.

At Grant Thornton, we have a team of suitably qualified individuals with the relevant expertise and experience to provide you with practical, cost-effective solutions to enhance the value creation of your captive. Our team’s extensive experience in industry and in supervision gives us a solid understanding of the requirements of captives and how to best support them in their strategic and operational ambitions.

Contact us

Explore our Insurance Risk & Actuarial solutions