Tax

Restricted share schemes

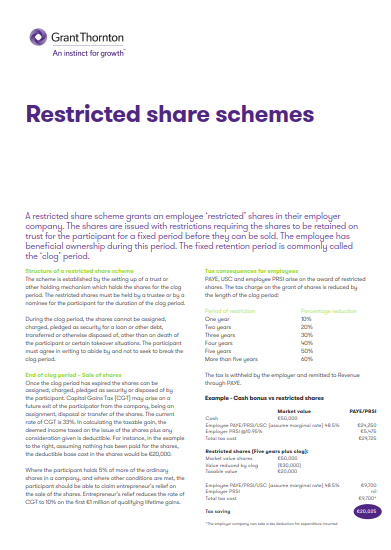

20 Feb 2019A restricted share scheme grants an employee “restricted” shares in their employer company. The shares are issued with restrictions requiring the shares to be retained on trust for the participant for a fixed period before they can be sold. The employee has beneficial ownership during this period. The fixed retention period is commonly called the ‘clog’ period.

In our document, we look at:

- structure of a restricted share scheme;

- end of clog period – sale of shares;

- tax consequences for employees;

- “good leaver/bad leaver” and sale of company; and

- company tax relief and reporting requirements.

Also appears under...