Amendments to IFRS 16 as a result of COVID-19

The International Accounting Standards Board (IASB) has issued amendments to IFRS 16 which simplifies how companies account for COVID-19-related rent concessions. IFRS 16 contains specific requirements on accounting for lease modifications including rent concessions that change the overall consideration for the lease. Lessees are required to assess whether rent concessions are lease modifications and, if they are, apply specific accounting guidance, which can be complex and burdensome. The simplification, otherwise referred to as the ‘practical expedient’ avoids the need for lessees to carry out an assessment to decide whether a COVID-19-related rent concession received is a lease modification or not. The practical expedient does not apply to lessors.

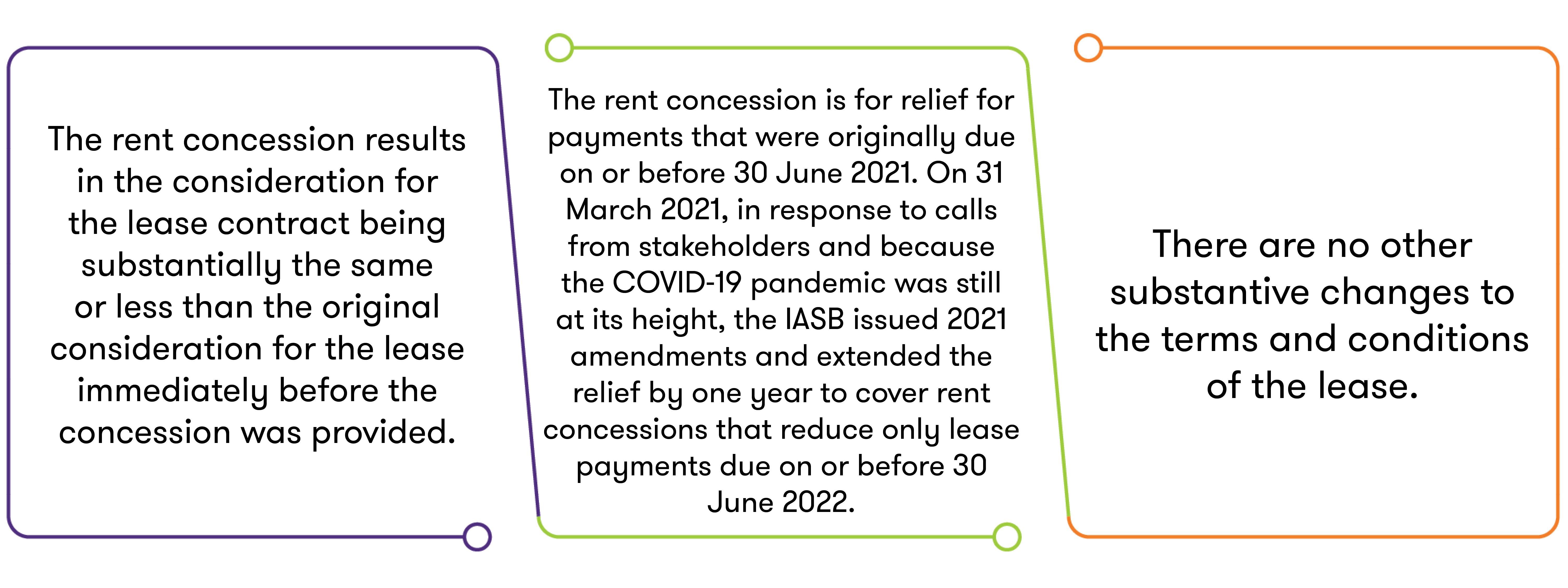

The practical expedient is only applicable to rent concessions provided as a direct result of the COVID-19 pandemic. In addition, the relief is only for lessees that are granted these rent concessions. All of the following conditions in relation to permitting a lessee to apply the practical expedient need to be met:

![Accounting for rent free first image.png]()

The 2020 amendments were applicable for reporting periods beginning on or after 1 June 2020. If the IASB had not extended the relief, the practical expedient would have expired by 30 June 2021. The 2021 amendments are effective for annual reporting periods beginning on or after 1 April 2021, however lessees are permitted to apply it early, including in financial statements not authorised for issue.

Lessees are not required to apply the practical expedient, it is optional. If the company choses to apply the practical expedient, the specific nature of the rent concession needs to be considered when accounting for it. Some practical examples of where the practical expedient might be used are where payments:

- are deferred for a period of time, and then increased at a future date

- are forgiven completely for a period of time

- are partly deferred and partly forgiven, and then partly increased at a future date.

If applying the practical expedient, the amendments require the entity to disclose:

- that it has applied the practical expedient to all its rent concessions, or if only some of them, a description of the nature of the contract it has applied the practical expedient to, and

- the amount in profit or loss for the reporting period that reflects the change in lease payments arising from rent concessions (as a result of applying the practical expedient).

Amendments to FRS 102 and FRS 105 as a result of COVID-19

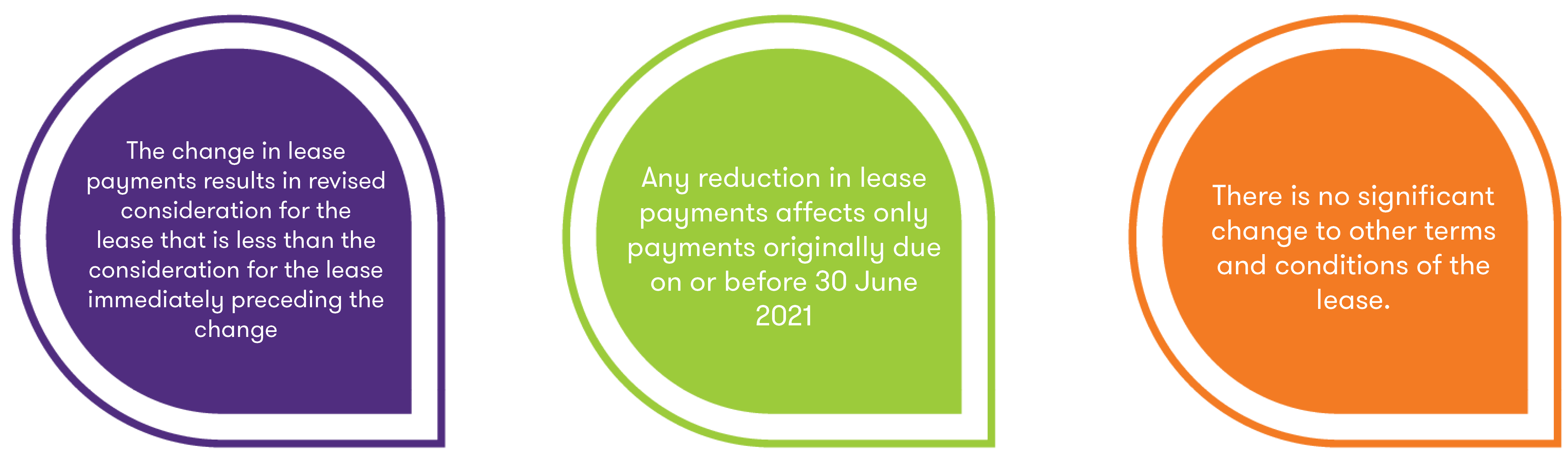

FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland does not explicitly specify how to account for changes in lease payments that result from rent concessions. This could have led to differences in accounting treatment for COVID-19-related rent concessions which would have been unhelpful to users of financial statements. In response to this, the FRC issued amendments to Section 20 Leases of FRS 102 which require entities to recognise changes in operating lease payments that arise from COVID-19-related rent concessions that meet the conditions (detailed below) on a systematic basis over the periods that the change in lease payments is intended to compensate. In comparison to the amendments to IFRS 16, the amendments to FRS 102 and FRS 105 are mandatory and applies to both lessees and lessors. A lessor shall recognise any change in lease income arising from rent concessions that meet the conditions (detailed below) on a systematic basis over the periods that the change in lease payments is intended to compensate.

Conditions to be met:

![Accounting for rent free 2nd image.png]()

The requirements apply only to temporary rent concessions occurring as a direct consequence of the COVID-19 pandemic and within a limited timeframe. The treatment is intended to reflect the economic substance of the benefit of these concessions and their temporary nature and improve the consistency of reporting for users of financial statements. Similar amendments are made to FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime. The effective date for these amendments is accounting periods beginning on or after 1 January 2020, with early application permitted.

On 20 April 2021, the FRC issued FRED 78 that proposes to extend the application period of requirements that cover the accounting treatment of temporary rent concessions occurring as a direct consequence of the COVID-19 pandemic by one year. FRED 78 proposes to extend the requirements originally introduced into FRS 102 and FRS 105 in October 2020 and apply to rent concessions that reduce only lease payments originally due on or before 30 June 2022, provided the other conditions for applying the requirements are met. The FRC says it expects to finalise these amendments in the first half of the year.

See our Audit offerings

![Subscribe button.jpg]()