Update your subscriptions for Grant Thornton publications and events.

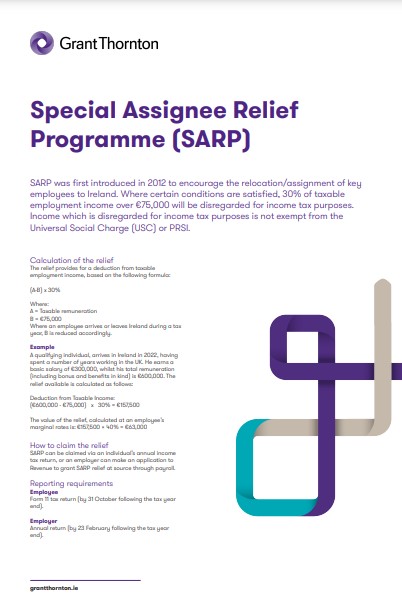

SARP was first introduced in 2012 to encourage the relocation/assignment of key

employees to Ireland.

Contents

Subscribe to our mailing list

Where certain conditions are satisfied, 30% of taxable employment income over €75,000 will be disregarded for income tax purposes. Income which is disregarded for income tax purposes is not exempt from the Universal Social Charge (USC) or PRSI.

In this update we look at:

- Calculation of the relief;

- How to claim the relief;

- Reporting requirements;

- Summary of conditions; and

- How Grant Thornton can help

Authors

-

Jillian O'Sullivan

Jillian is a partner in Grant Thornton, as part of her role she leads the Company Secretarial offering for Grant Thornton Ireland, one of the leading professional services firms in Ireland.View Profile -

Jane Quirke

Jane is a director in tax in our employer's solutions team in Ireland. She has significant experience advising clients from start-ups to large Irish indigenous and listed multinational companies on employment tax related matters.View Profile