Going Concern - Responsibilities of Management and directors

14 Jun 2021The financial reporting frameworks applicable in Ireland generally require the adoption of the going concern basis of accounting in financial statements, except in circumstances where management intends to liquidate the Company or to cease trading, or has no realistic alternative to liquidation or cessation of operations.

In some circumstances, material uncertainties may exist which may cast significant doubt about the ability of the Company to continue as a going concern. If this is the case, it is the responsibility of management to outline the details of these uncertainties and their potential impact on the financial statements as a whole.

Given the impact of the Covid-19 Pandemic (Covid) on the domestic and wider global economy there is a greater emphasis on boards of directors to set out clearly to the users of their financial statements, including shareholders and auditors, why they are satisfied that the financial statements should be prepared on a going concern basis.

Many sectors, including hospitality and retail, have been severely impacted by Covid and therefore the task of the directors to assess going concern can prove very challenging indeed.

Under Company law in Ireland, a Company is presumed to be carrying on business as a going concern. However, the accounting frameworks (IFRS and Irish GAAP) impose a requirement for directors to assess the ability of a Company to continue as a going concern. Directors need to satisfy themselves, shareholders and auditors that, having considered all available information about the future, the Company has sufficient cash resources and/or funding facilities to trade and to pay their debts as they fall due for a period, not limited to, but of no less than 12 months ahead. For emphasis, the 12 month timeline is only a minimum requirement, in that if the directors do not believe that ultimately they will be able to discharge the Company’s short and long term debts (i.e. including debts payable after 12 months) then immediate action needs to be taken by the board to protect all stakeholders of the Company.

If the directors cannot assess the ability of the Company to continue as a going concern with reasonable certainty, then they should take adequate steps to assess the solvency of the Company. If necessary, they should take all reasonable action to protect the creditors and shareholders of the Company from any further exposure that would result from trading in a reckless manner.

In the event of a situation where the directors of a Company continue to trade in a reckless manner, there are provisions under the Companies Acts which set out the penalties for doing so.

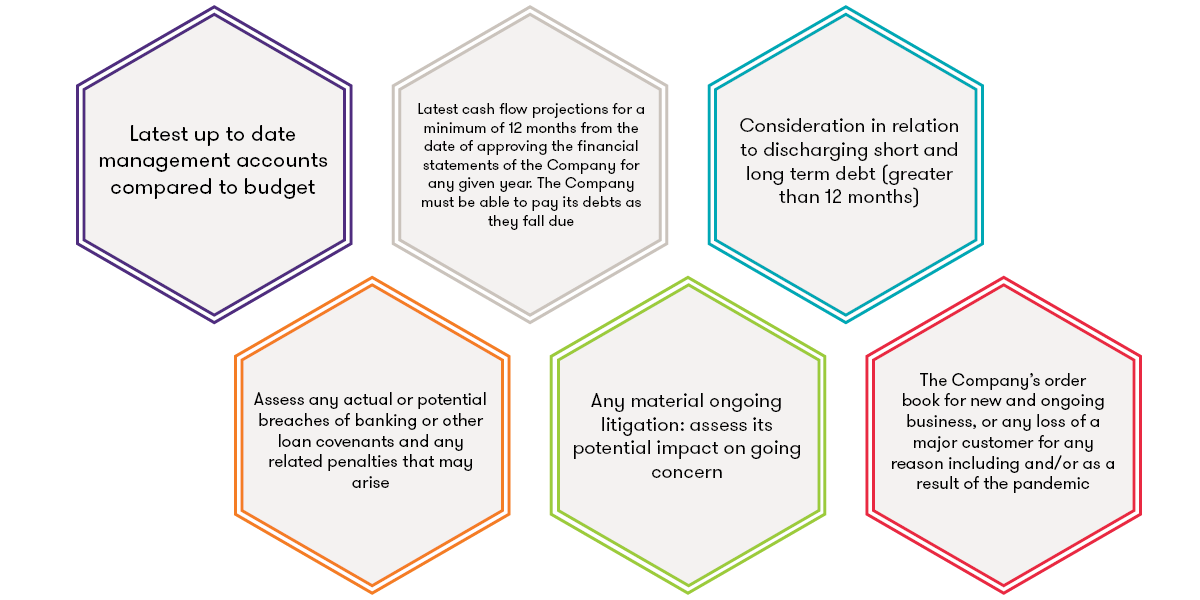

In assessing going concern the directors should consider the following:

The above list is only a sample of the issues that the board needs to consider in relation to discharging their responsibilities in relation to going concern. There may and probably will be others.

It is also worth noting that the recent changes to International Standard on Auditing 570, Going concern, place greater responsibilities on the auditor in respect of procedures to be undertaken and reporting on the Company’s ability to continue as a going concern. The auditor’s obligation has changed from a “we have nothing to report” approach to “we have concluded… based on the work we have performed”. This change to a positive opinion will ultimately result in greater scrutiny of the going concern assumption by auditors, which will most likely lead to an increased workload on management and auditors alike.

Finally, we recommend that management engage with its auditors early on in the audit process to front load the work that will be required to conclude on going concern. Be prepared for a greater amount of focus on going concern.

If you have any questions in relation to management and directors’ obligations relating to going concern, please contact a member of your GT client services team.