On 24 April 2023, the European Central Bank (ECB) and European Insurance and Occupational Pensions Authority (EIOPA) published their joint discussion paper on possible actions that can be taken to reduce the climate insurance protection gap and mitigate climate-related catastrophe risks in the EU.

The paper explores the tools available to consumers, (re)insurers and governments for minimising the economic effects of these weather-related events so that they can be better quantified and in turn more manageable.

The protection gap is measured as the estimated level of risk from each type of catastrophe risk compared to the estimated insurance penetration, i.e. the amount of the risk insured for that risk. The discussion paper considers flood, coastal flood, earthquake, wildfire, and windstorm risks. With some (re)insurers reducing their appetite for, or withdrawing entirely from, certain types of catastrophe (re)insurance, the protection gap may widen at an accelerated rate.

The macroeconomic impact of these weather-related events is also expected to worsen as their frequency and severity increases because of climate change. The impact of these events is two-fold: the initial destruction that an event causes combined with delays in reconstruction that result in delayed recovery of economic activity.

This effect is more pronounced in areas of low insurance penetration where those not covered by private insurance may need to use their own savings or credit facilities to finance post-disaster reconstruction, or they may rely on government relief—the extent of which can be uncertain—that often results in a lengthier process than an insurance claim payment.

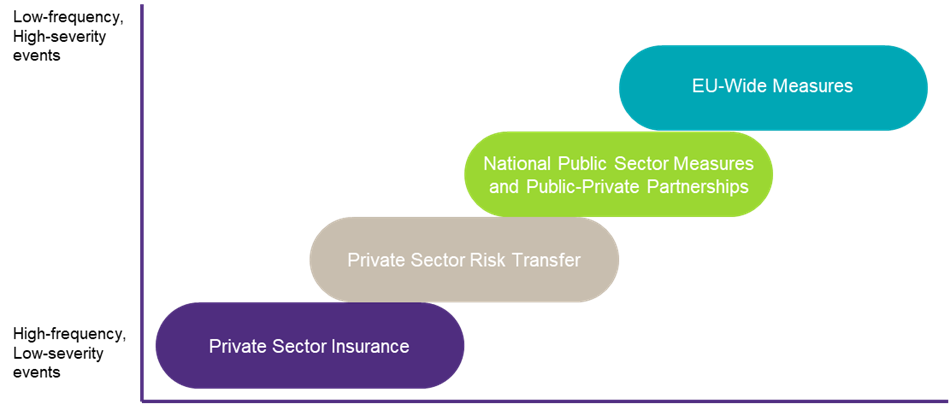

The ECB and EIOPA’s Ladder Approach

The discussion paper outlines a ‘Ladder Approach’ to catastrophe insurance as a method for bridging the protection gap in EU member states. The approach sets out a combination of potential policy measures to help reduce the protection gap and mitigate climate catastrophe risks across all stakeholders.

![ladder approach graph]()

Prviate Sector: Recommendations to Reduce Climate Insurance Protection Gap

For insurance policies that protect against climate risks, the discussion paper recommends that providers design these policies to incentivise policyholders to adopt risk mitigation and adaptation measures through premium reductions. Such strategic measures are known as impact underwriting. For example, a provider may offer a premium reduction to a home insurance policyholder in a flood-prone area if their home meets certain flood-proofing standards.

The use of impact underwriting can raise policyholder awareness of their exposure to climate risks. The discussion paper mentions that targeted information campaigns may also be useful to make policyholders aware of their climate risk exposure at a local level, for instance, a web-based tool of flood-risk levels.

Challenges of Reducing the Climate Protection Insurance Gap for Reinsurance

One measure raised for traditional catastrophe reinsurance is the use of multi-year contracts with terms of three to 25 years instead of the standard one-year term. The discussion paper argues that the annualised nature of structuring and pricing does little to encourage the incorporation of climate change considerations into reinsurance program structuring because there is always a “short cut” of adjusting the premium after one year.

The paper also cites SwissRe’s estimation that global catastrophe losses in 2022 amounted to 120 billion USD; therefore, it is reasonable to acknowledge that any type of longer-term view would be unsustainable for reinsurers. It is becoming increasingly difficult for catastrophe models, which reinsurers rely upon for pricing and structuring to robustly capture the physics of climate change, to adequately evaluate and price reinsurance coverage.

Given this level of uncertainty, reinsurers prefer to refine their pricing year on year, which gives them the opportunity to receive some payback for losses suffered during the previous years. As a result, it is likely that any multi-year coverage offered would be prohibitively expensive for ceding insurers.

Insurance-Linked Securities: Cat Bonds as an Alternative Method of Risk Transfer for (Re)insurers

The paper also analyses cat bonds as an alternative method of risk transfer for (re)insurers. Cat bonds allow for catastrophe risk to be transferred to the capital markets that benefit from diversification. Cat bonds can also be subject to supply-driven volatility, with capital market investors being less likely to offer affordable coverage in a hard market than traditional reinsurers.

High transaction costs associated with issuing cat bonds, which include setting up a special purpose vehicle (SPV), hiring independent modelling agents and marketing securities, may also be a deterrent to their wider use in risk transfer. However, given that Irish tax legislation provides for special tax treatment in relation to qualifying SPVs and (re)insurers benefit from Solvency II jurisdiction, a number of existing SPVs are domiciled in Ireland for the purposes of issuing US and some European cat bonds, set up by larger global (re)insurers

Furthermore, the paper provides examples of other jurisdictions’ moves to attract issuers of cat bonds. In Bermuda, the licensing and registration process for entities to issue insurance-linked securities (ILS) is now completed within three days. In Hong Kong, a pilot scheme was introduced in 2021 to incentivise ILS, and a separate scheme offers a grant to cover the upfront expenses for certain ILS. A similar grant scheme has also been introduced in Singapore.

Whilst cat bonds are interesting and could offer a useful risk-transfer method alongside traditional (re)insurance structures, their volatility, cost and complex setup means they are normally more suitable for larger (often global) (re)insurers in European markets. This discussion paper does, however, propose the option of cat bond issuance by the public sector, which could operate on a multi country basis thereby lowering operational costs.

Over time, this option would allow for modelled outputs and pricing gathered as part of the issuance process, driving efficiencies in future issuances and helping to inform policymaking on natural disaster risk financing at a national & EU level.

National Measures for Reducing the Protection Gap

At a national level, governments can take steps to reduce the protection gap by encouraging uptake of private insurance against climate risks. Current disaster relief is largely set out post-event and is unconditional, which can create moral hazard since homeowners have less incentive to purchase insurance against natural disasters if state disaster relief is likely to cover such perils.

By setting out which perils will and will not be covered by its disaster relief prior to catastrophe events, the state can help households understand the risks that will be covered and those that will require private protection.

The public sector can also take measures to reduce the protection gap. National reserve funds and public-private partnerships (PPPs) can enhance the state’s disaster risk management strategy. PPPs are already in place in France, Spain and other EU member states. The state guaranteed Caisse Centrale de Réassurance (CCR) scheme in France provides reinsurance for natural disaster risks after catastrophe event occurs and undergoes an assessment process in order to be publicly declared as covered under the scheme.

To be eligible for compensation from this scheme, the damage must be covered by private insurance, which means the CCR operates as a catastrophe reinsurance scheme rather than a blanket disaster relief mechanism. The discussion paper notes that while these schemes can bridge the protection gap for climate catastrophes, they have the potential to subsidise property development in hazardous locations, such as flood plains, thereby increasing residual risk.

European Union Measures for Reducing the Protection Gap

The discussion paper suggests that an EU-wide public scheme could complement these national measures. It points out that it may be cost efficient to pool risks at this level, given that the lowest-frequency high-severity disasters are likely to be weakly correlated across the EU.

This scheme would ensure that in the event of large-scale climate disasters, adequate funds are available to member states to accelerate recovery and reconstruction efforts. The funds of such a scheme could also be invested in liquid investment grade green bonds thereby allowing the fund to support the complimentary efforts of mitigating climate change and reducing global warming.

Conclusion: Europe Needs to Close the Climate Insurance Protection Gap

With only a quarter of climate-related losses currently covered in Europe, governments are having to respond to this protection gap. Governments and (re)insurers should build awareness of and explore the options above to help reduce this gap as climate catastrophes become both more frequent and severe. By implementing some of these measures, losses caused by these disasters and subsequent disruption to economic activity may become more manageable and more quantifiable.

What Next?

The ECB and EIOPA are seeking industry feedback on the discussion paper, which should be sent to ecb_eiopa_staff_protection_gap@eiopa.eu by 15th June 2023.

How Grant Thornton Can Help

Grant Thornton’s financial services risk, consulting and advisory teams are comprised of dedicated experts who have extensive experience in supporting insurance firms with a variety of challenges including those arising from the ESG agenda.

In particular, our industry-leading prudential risk team and our ESG and climate risk experts understand that the climate insurance protection gap will be a driver of the strategic agenda for (re)insurance firms and other stakeholders. ESG and other sustainability-related areas are likely to be high on (re)insurer’s and government’s outlooks for years to come.

Our expert teams specialise in assisting clients across the financial services sector in navigating climate-related risk challenges and supporting them in identifying regulatory obligations and working towards full compliance balanced with their business needs.