MOSS

The Mini One Stop Shop, better known as MOSS, is a simplification measure to reduce the administrative burden and costs for businesses should they be in involved in supplying telecommunications, broadcasting and electronic (TBE) services to non-taxable persons i.e. typically private consumers.

A business files a quarterly return to report these TBE sales for all EU member states in one EU Member State, known as the Member State of Identification. This is strictly an intra-EU mechanism and supplies outside the EU are not included.

With the UK leaving the EU in 2021, this has many implications for UK businesses that operate MOSS.

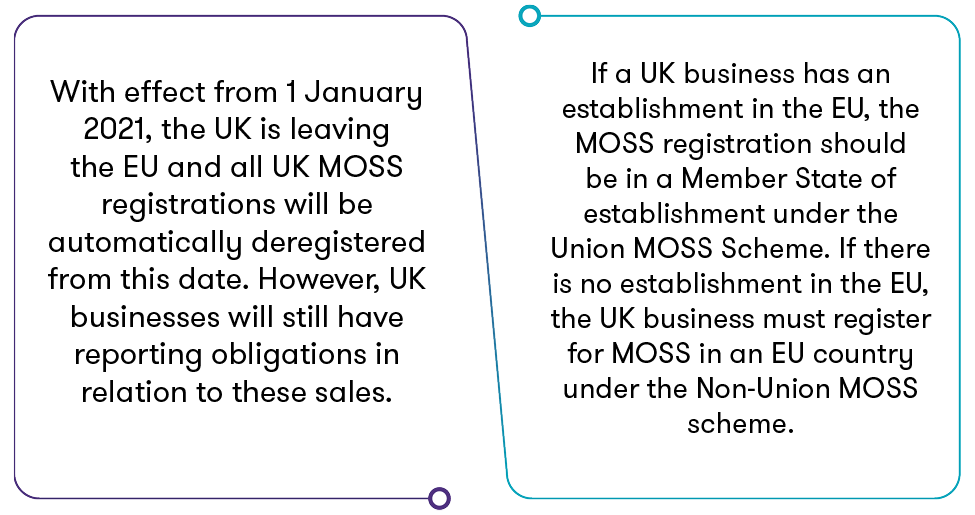

Post Brexit

![3POST BREXIT.png]()

What is the Non-Union MOSS Scheme?

This scheme applies to any business which is established outside the EU supplying the above business to consumer i.e. B2C of TBE services.

How will the UK report these sales now?

Provided the UK does not have an establishment in an EU Member State, the UK business can choose any jurisdiction to register for MOSS and in this regard Ireland has been an attractive location.

The deadline for this registration for MOSS in Ireland or any EU country as the chosen jurisdiction is the 10th day of the month following the first sale to an EU based customer. For example: A sale is made to a French customer on 13 January 2021. A Non-Union MOSS registration must be made by 10 February 2021.

Businesses should ensure that the IT systems and software are capable of accommodating this change.

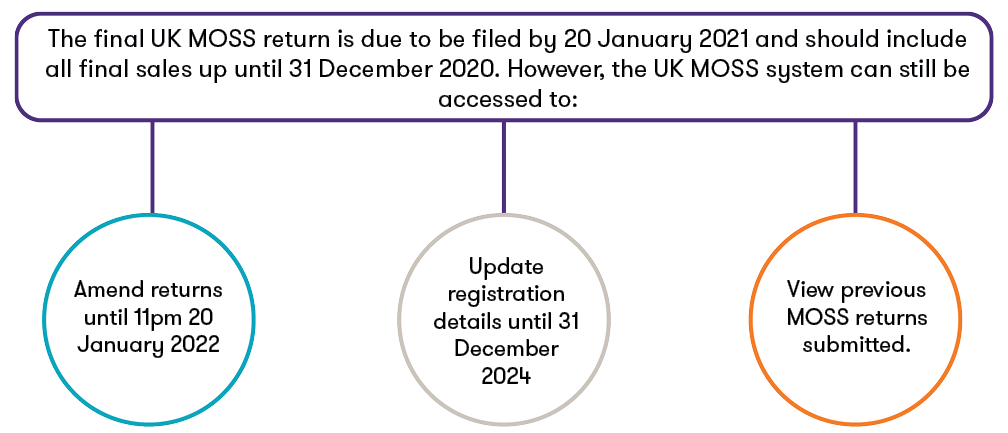

UK MOSS System

![2UK MOSS SYSTEM.png]()

Therefore post automatically deregistration, the UK business can still access UK MOSS during the above time frame for these specific actions.

What to do now?

Should your business wish to register for MOSS in Ireland, please get in contact with the Grant Thornton VAT team presented below.

![Subscribe button.jpg]()